The time value of money refers to the principle that money in the future will have a different value (or buying power) than the same amount of money today. The change in value is largely due to inflation and interest earned through investments. For example, if I have a savings account that provides 5% interest, then $100 invested today will be worth $105 in one year.

To illustrate the time value of inflation, use the Bureau of Labor Statistic's inflation calculator to calculate the difference in value for $10 in 1980 versus 2013. (Click on the icon below)

We call the interest rate that is used to determine the future value of

a stream of payments or cash flow the discount rate. The discount

rate is normally based on the interest rate charged by the Federal Reserve

to member banks. (Or, the desired return (interest) rate on an investment)

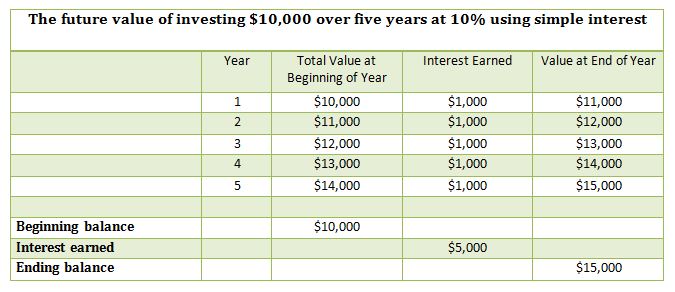

Let's look at an example of an investment of $10,000 at 10% interest

at the end of five years. Using simple interest, the interest earned is calculated each year

on the original investment amount of $10,000. At the end of five years, the value is $15,000.

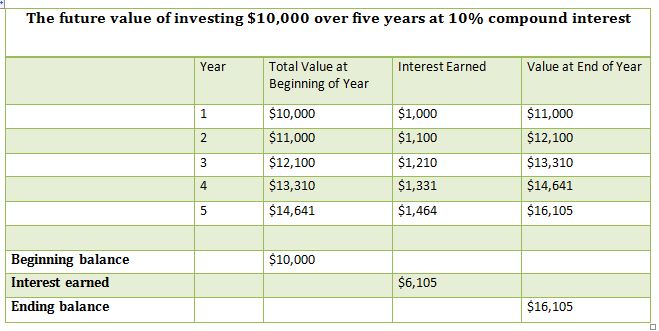

Most of the time, interest earned on investments is calculated on both the original investment amount plus the added interest. This is called compound interest. In the chart below, you can see that investments earning compound interest gain at a higher value after a period of time.

Let's see what the Khan Academy has to say about the time value of money.

Click on the icon below.